The insurance industry has long had to adapt to ever-changing economic and societal conditions, updating and reassessing risks and premiums regularly.

But there is one factor that insurers will never be able to control, no matter how hard they try: the weather.

The weather is often unpredictable and there are always unusual storms and unexpected impacts on your customers. Insurers today need to better manage and mitigate the risk posed by weather events or face potentially huge losses.

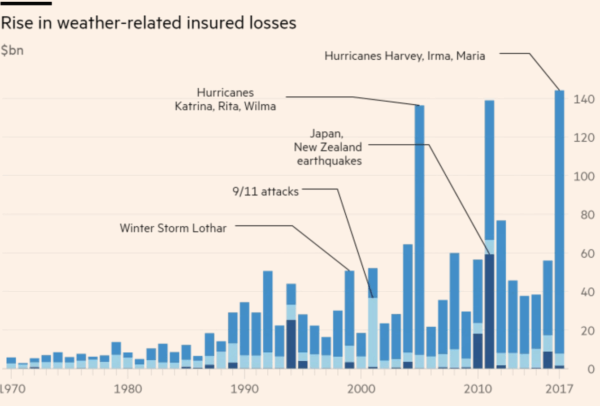

The losses suffered by insurance companies because of major weather events have been well documented, and no state or country is immune:

- Hurricanes Florence and Michael, which hit the US in the second half of 2018, resulted in insured losses of more than $10 billion.

- The extreme freeze that hit the UK early in 2018 resulted in insurers paying a record amount of £194million in three months for burst pipes.

- In 2019, at least two of Australia’s leading insurers used up their full-year allowance in just 6 months due to natural disasters.

- In 2017, Hurricanes Harvey, Irma, and Maria pushed weather-related insured losses for that year to more than $140 billion.

The situation is only likely to get worse if insurers don’t act now to improve their ability to adapt to the changing climate. In fact, analysts predicting that the average annual severe weather claims paid by insurers could more than double over the next 10 years.

Learn how today’s top insurers are shifting their thinking when it comes to the weather, and making smarter, more data-driven decisions.

New Risk and Secondary Perils

Weather-related risk manifests in different ways according to climate, geographical characteristics, and urban sprawl.

Insurers have long been dealing with claims due to local flooding, prolonged drought, and torrential rain for some time. Yet, a changing climate and population growth in areas of high exposure are adding to the complexity of covering weather-related damage. As the global climate evolves, some risks become more prominent, and insurers don’t have sufficient models to understand and mitigate the resulting risk.

Take wildfires, for example. In 2020, Hiscox, an underwriter at the insurance market Lloyd’s of London, paid to license a risk model for wildfires in the United States. Shree Khare, head of catastrophe research at the company, said that it will help Hiscox set premiums more accurately and that without the model it might otherwise have stopped insuring some clients in high-risk areas.

Khare explained the industry’s often reactive approach to new developments:

“Prior to this year, we didn’t really have a good modeling solution for U.S. wildfires. I think it’s just the nature of insurance. We tend to worry about things after they happen.”

The proof of the ever-changing nature of weather-related risk came when the California wildfires dominated the headlines in summer 2020. Just two wildfires in California cost insurers between $9 billion and $13 billion alone.

The need to shift focus is part of a trend. According to reinsurance firm Swiss Re, natural catastrophe losses from primary perils are overtaken by those traditionally considered secondary. Secondary perils are small-to-midsize weather events or the secondary effects of a primary peril. These include weather events such as:

- Wildfires

- Flash floods

- Hail

The secondary effects of a primary peril include:

- Property losses for structural damage

- The expense of living costs while the home is being repaired or rebuilt

- Commercial losses, such as loss of income

Thierry Corti, head of climate change strategy a reinsurance firm Swiss Re, reports that secondary perils are very localized and short-term.

“We really need to understand them on a case-by-case basis and it’s often very hard to generalize.”

To stay on top of these threats, insurers need access to localized, real-time data if they are to mitigate risks and afford to stay in business.

The Soaring Price of Premiums

The ability to adapt quickly to new risks is part of the nature of the industry. But with uncertainty around the changing climate and differing weather-related risks, it can expose insurers to large losses.

If firms are unable to mitigate these losses and put away enough money to protect their business, they will have to raise premiums or pull coverage from higher-risk areas. Home insurance coverage is already higher in Florida, for example, a state which is prone to hurricanes, than in countries in Northern Europe where hurricanes are rare. And with 2020’s record-breaking hurricane season, this is only likely to increase.

This throws up a further curveball of affordability. Rising premiums could put insurance out of reach for many customers, especially as insurers’ predictions of their natural hazard allowance are often not adequate.

You can start to see signs of these issues when analyzing losses that are not covered by insurance. Swiss Re estimated that insurance only covered about half of 2018’s economic losses from natural and man-made disasters.

The California Department of Insurance regulator reported in August 2020 that insurance coverage was becoming harder to find for communities prone to wildfire. There had also been a 10% increase in insurers refusing to renew policies last year in areas that were affected by fires in 2015 and 2017.

One issue that is driving these price increases is the lack of weather insights. Insurers are too often failing to work with meteorologists and climate change specialists regularly to harness the insights they can provide. Instead, they take an ad hoc approach, only tapping into available expertise in the wake of an incident.

Stephan Harrison, director of consultancy Climate Change Risk Management, believes that lack of collaboration with meteorological experts prevents insurers from accurately pricing insurance coverage. He explained:

“Insurers tend to consult us on an ad-hoc basis without really having a handle on climate change and the risks it poses to infrastructure.”

However, as extreme and everyday weather continues to evolve, insurers need up-to-date data and a way to get actionable insight into local weather events and long-term changes in the climate if they are to provide affordable coverage, mitigate risk, and manage their losses.

Relying on Historical Weather Data

Many insurance companies still assume the risk to property from extreme weather is static. They base their premiums on historical weather data, rather than more recent insight updated for the ever-changing climate.

Given that extreme weather events are increasing in severity, frequency, and unpredictability, insurers need to put available weather data to better use.

According to Jason Thistlethwaite, a climate change economist at the University of Waterloo:

“As extreme events become more frequent, insurers that ignore climate change will not put away enough money to cover their claims. To recoup those losses, they’ll have to raise rates or pull coverage from high-risk areas. When this shift happens, thousands of people will lose coverage or it will be unaffordable.”

According to Deloitte, the uncertainty of a changing climate, combined with the diversity and rising frequency of perils, may make historical loss data that the insurance industry relies on for its catastrophe modeling less useful for future loss projections.

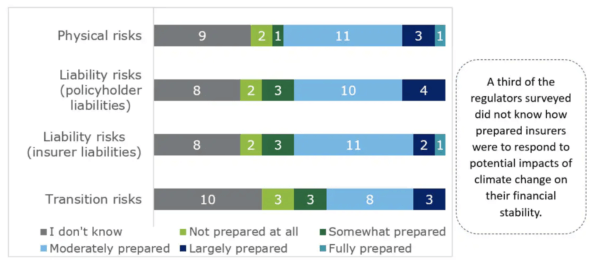

Deloitte also reports that regulators also aren’t confident that insurers are adequately prepared to respond to the potential impacts of climate-related risks.

The Power of Predictive Weather Intelligence

While current trends may point to a much more expensive future for insurers, this does not have to be the case.

Instead, insurers need to better understand the risks, how they are changing, and what that means for their customers. They have to rethink traditional models that are not suitable for the current climate. Proactive risk management is required to minimize losses due to current and future weather events, and get ahead of the weather. The insurance industry needs to utilize hyper-local weather data to more accurately price insurance cover and continue to offer affordable premiums to customers.

While insurers need to understand what is going to happen in the immediate future in specific locations, they also need insight into the longer-term weather predictions so they can accurately price coverage. They need to take into account climate as well as weather and understand how that will affect the way they price contracts for consumers. For example, with more houses being built along Florida’s coast that could end up being underwater, how will that affect the price of the insurance they offer?

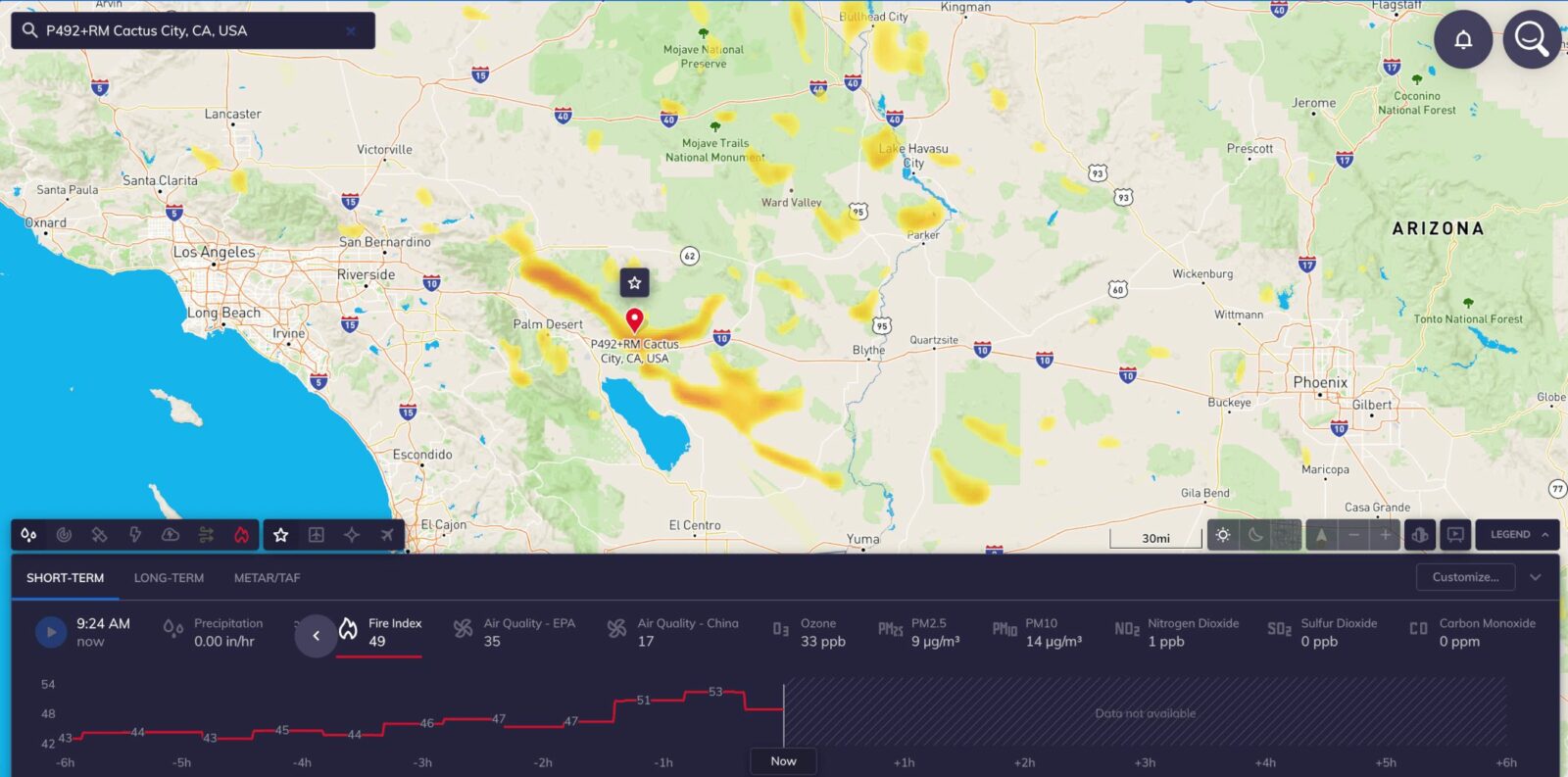

Weather intelligence software provides the level of insight necessary to make these decisions. Tomorrow.io’s Weather Intelligence platform provides predictive and customized weather insights that enable you to get the right information to drive actions that directly impact revenue.

It can validate claims with hyperlocal historical weather data and let insurers know in advance where there’s likely to be high wind, hail, and even tornadoes. The intuitive dashboard provides observational data in real-time for specific locations, which you can combine with historical data to better prejudice what will happen in the future.

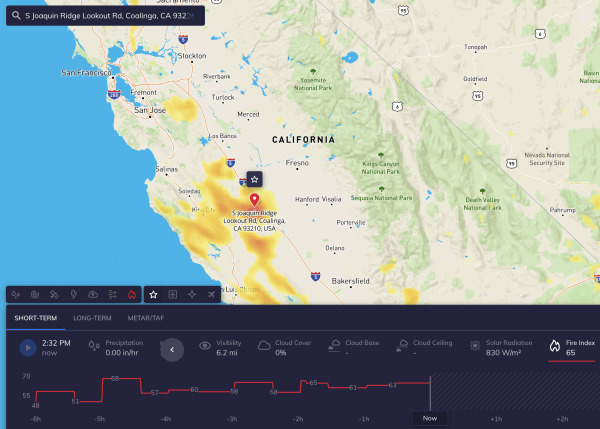

Take the Fire Index feature, which provides data on the average wildfire risk for the exact location, given average climate conditions in the past 20 years. This can help insurers understand the general fire risk profile for each location on the globe.

The platform also provides customized flood alerts, which predict urban floods up to 36 hours before they occur. This can help insurers more accurately estimate claim counts and amounts.

Preventative Weather Alerts

It’s not only about preventing loss, but also proactively serving your customers. More extreme weather events do not have to lead to less profit if you have a system in place to warn consumers about risks and advise them what to do to avoid damage.

A report from KPMG states that:

“The insurance industry and policy makers are increasingly recognizing that while historically the insurance model has been built around protecting policy holders from loss, going forward the new business model will have to rely much more on preventing the loss in the first place.”

With weather intelligence technology, you can set up preventative alerts to monitor the specific locations where your customers live.

These preventative weather alerts help policyholders avoid potentially damaging weather events. If your policyholders live in the path of an incoming storm, for example, you can send them alerts directly through an app or via email. You can prevent a large number of claims by helping your customers stay safe during storms.

Insurers can use this insight to take a long-term approach that results in improved customer satisfaction and fewer payouts.

Here are some proactive alerts you can send:

- Hail: Tell every policyholder in that zip code to move their cars indoors before they’re damaged by the hail.

- High winds: Alert consumers to potentially damaging winds and allow them to secure property that is at risk.

- Wildfires: Make sure customers are aware of the risks and can create a safe zone around properties.

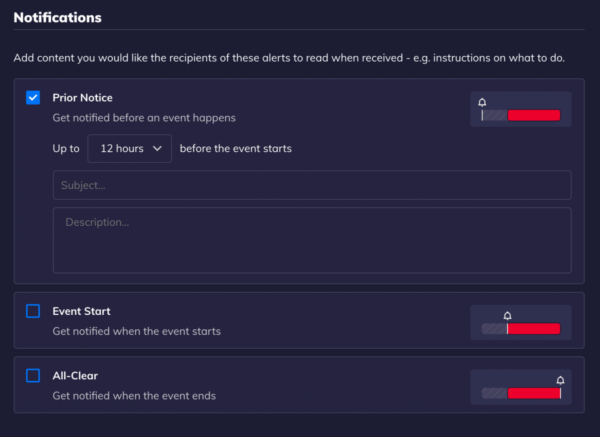

Alerts are only sent when it matters, such as:

- Prior to the weather event occurring

- When the event begins

- When the event ends

Customization settings also allow you to send alerts based on the time zone of the recipient.

Save Money, Boost Customer Satisfaction

A major insurance company recently leveraged Tomorrow.io’s preventative weather alerts to help reduce road risk by telling insured drivers about incoming weather. The alerts were sent out in advance of heavy snow, freezing rain, hail, rain, and strong winds.

The company saved an average of $3,000 per hail claim and 90% of customers said they were happy with the content they were receiving via phone notifications. Drivers took action after receiving alerts to better protect themselves and their vehicles, and the program is on track to generate tens of millions in cost savings and new revenue opportunities.

The insurance company was also able to:

- Improve customer trust and retention

- Increase customer engagement

- Develop more upselling opportunities

- Identify a new, repeatable, and scalable sales strategy

Weather alerts are of immense value when it comes to both saving money and keeping customers happy. And, as this insurance company found, if you can increase customer satisfaction and retention by even just a few percentage points, that can lead to millions of dollars in value in the coming years.

See How Tomorrow.io Can Help