How pre-loss decision systems are becoming a combined ratio lever for North America’s largest auto carriers

Three years in the making. Purpose-built for P&C carriers looking to improve loss ratios while creating a new form of policyholder engagement. Shield is Tomorrow.io’s preventative notifications product — refined through multiple years of satellites launched, models trained, and feedback collected with some of the largest carriers in North America, during the costliest three-year hail period on record.

The Problem

Hail is no longer a weather event. It is a recurring earnings drag.

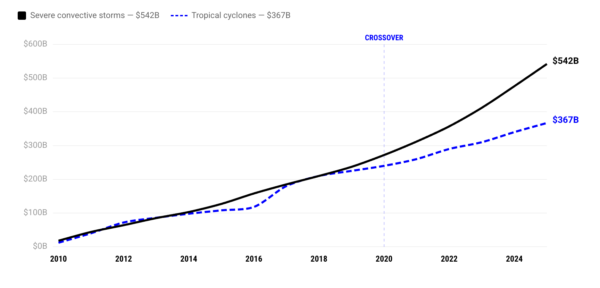

Severe convective storms have surpassed tropical cyclones as the costliest insured peril of the 21st century. Since 2010, SCS has generated $542 billion in insured losses globally, compared to $367 billion from tropical cyclones. In 2025 alone, SCS produced $61 billion in insured losses — the third consecutive year above $45 billion.

Sources: Gallagher Re, May 2025; Aon 2026 Climate and Catastrophe Insight Report.

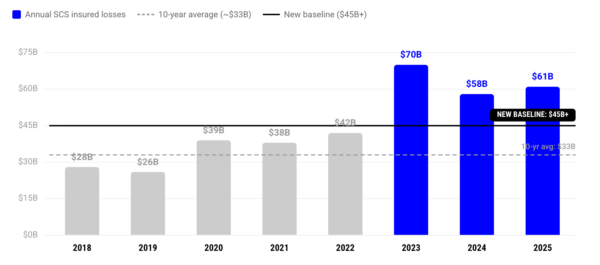

This is no longer volatility. Moody’s 2025 Catastrophe Review concluded that a $45 billion annual SCS loss “has transformed from an anomaly into a new baseline.” Hail accounts for 50–80% of all SCS losses, making it the dominant sub-peril within the dominant peril category.

Sources: Moody’s Insights, 2026; Allianz Commercial, April 2026.

The executives running the largest personal auto books in North America are not treating this as episodic. They are describing it as structural:

“A fast-moving hailstorm earlier this year cost $370 million in insured losses, the single largest weather event in our company’s history.”

“We’ve seen absolute record numbers of events and the cost to repair that has been significant.”

In 2023, American Family reported $3.5 billion in catastrophe claims driven by hail and wind, producing a combined ratio of 110.8% and a net underwriting loss of $1.7 billion. In May 2024 alone, Allstate incurred $1.48 billion in catastrophe losses, with approximately 70% attributable to five hail and wind events in Texas, Colorado, and Illinois. Progressive burned through $722 million in net catastrophe losses in a single month — 12.3 loss ratio points — and was close to exhausting its annual aggregate reinsurance retention by the end of May.

Sources: American Family Newsroom; Allstate SEC 8-K, June 2024; Progressive SEC 8-K, May 2024.

Every carrier in the top 20 is managing this through pricing, reserve adjustments, and reinsurance restructuring. Almost none are managing it through loss prevention — despite it being the only lever that reduces the loss itself, not just the exposure to it.

The Structural Gap

Why this sits on your balance sheet — not your reinsurer’s

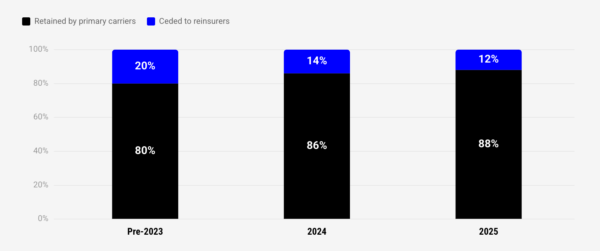

There is a structural reason hail losses hit primary carriers so hard: reinsurers have largely exited the layer where SCS lives.

Before 2023, reinsurers absorbed approximately 20% of global insured catastrophe losses. In 2025, that share fell to 12% — a 40% collapse in three years. Traditional reinsurance capital has moved away from providing coverage at the 1-in-3 to 1-in-5 year event level, attaching instead around 1-in-10 year events. SCS — frequent, moderate-severity, geographically dispersed — falls below the floor.

Sources: Guy Carpenter / S&P Global Market Intelligence, Jan 2026; Gallagher Re, 2024; FSI/IAIS Report, March 2025.

We’ve estimated $154 billion in cat losses. The reality is reinsurance has not picked up much of it.”

“The most important thing is that the retentions held. Retentions are the piece that allows us to continue to construct a portfolio and be removed from attritional losses, and that’s the most important thing that we’re focused on.”

The FSI and IAIS confirmed this in a 2025 supervisory report: “The low share of risk transferred to the largest 19 reinsurers is mainly because many secondary perils, including hailstorms and convective storms, caused property losses that were too small to be covered in reinsurance.”

The bottom line

This is not a market cycle. It is a structural redesign of how reinsurance capital deploys.

Rates are softening, but attachment points and retentions have held firm. For most personal auto carriers, hail losses are fully retained.

The exposure sits on the primary carrier’s balance sheet.

The flip side: reinsurers are rewarding mitigation

Aon’s July 2025 renewal report found that reinsurers “showed greater confidence in those cedants who articulated the actions they have taken to improve performance.” Cedants who could not provide that evidence received less favorable terms.

Source: Aon Reinsurance Market Dynamics, July 2025.

Guy Carpenter reinforced this: carriers must “sharpen underwriting strategies and improve exposure data” to make their SCS portfolios attractive to reinsurers. The message is clear — demonstrable loss mitigation is becoming a factor in reinsurance pricing, not just a claims management talking point.

Any lever that demonstrably reduces retained SCS losses is not a product — it is a capital strategy tool. It changes the conversation at your next reinsurance renewal.

The Math

Quantifying the lever: the 160-basis-point math

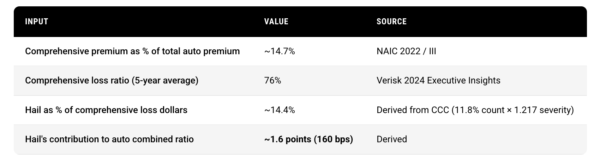

Hail’s impact on the personal auto combined ratio can be derived from publicly available data:

Note: The 14.4% hail share is derived from CCC claim count and severity data, not a directly published figure. Readers can validate against their own book.

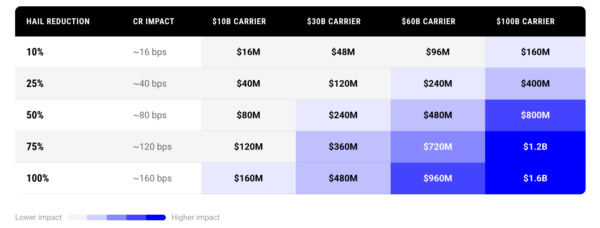

What does a reduction in hail claims mean at the portfolio level?

Based on indemnity-only claim costs. Fully loaded costs (adjuster, rental, admin) are 35-70% higher — making these figures conservative. For hail-belt-concentrated carriers, multiply by 1.5-2x.

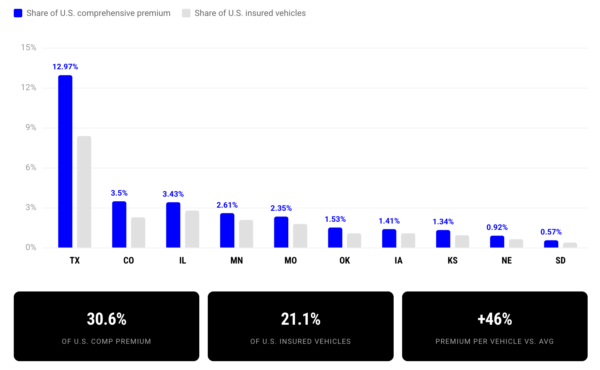

These figures assume national averages. For carriers with outsized hail-belt exposure — Texas alone represents 13% of all U.S. comprehensive premium — the per-book impact is materially higher.

The unit economics beneath the math

The average auto hail claim costs $4,000–$5,000, with hail claims running 21.7% costlier than the average comprehensive claim. Comprehensive claim severity at the $500 deductible has increased 74% over five years — from $1,392 to $2,417.

These figures reflect indemnity alone. The fully loaded cost per hail claim — including adjuster deployment, rental car coordination, and administrative processing — reaches $5,000–$6,850 in normal periods and $6,150–$8,500 during surge, when independent adjuster day rates exceed $500 and repair cycle times extend to 34 days.

Sources: III; CCC Crash Course Q2 2024; Verisk 2024; J.D. Power 2024; AdjusterPro fee schedules.

The Precision Gap

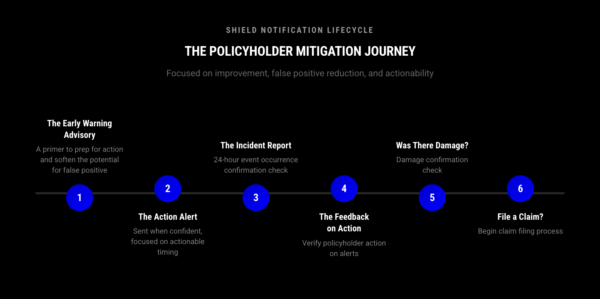

From advisory to action: the evolution of pre-loss notification

A pre-loss hail notification program is simple in concept — alert policyholders before a hailstorm reaches their location so they can move vehicles to covered parking. The financial logic is straightforward: a moved car is a claim that never happens.

Several carriers have attempted this over the past decade. Most saw early engagement collapse within seasons. The issue was never the idea. It was the forecast.

National weather advisory systems are designed, correctly, to protect citizens at scale. When public safety is the mission, the acceptable failure mode is a false negative. False positives are a tolerable cost. For insurance carriers trying to drive policyholder action, that tradeoff erodes trust quickly.

Built for citizen safety

- Wide geographic coverage

- Broad time windows

- Optimized to never miss an event

- Policyholders act, nothing happens, they stop listening

Built for loss ratios

- Address-level, peril-specific forecasting

- Strategic timing calibrated to maximize action

- Calibrated probabilities that sustain trust

- Policyholders trust and respond when it matters

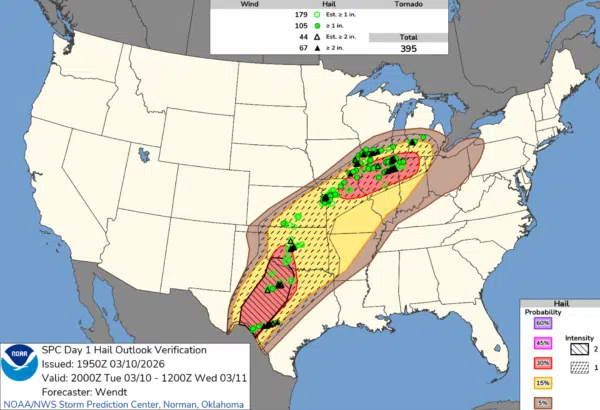

NWS / SPC Broad-Coverage Advisory

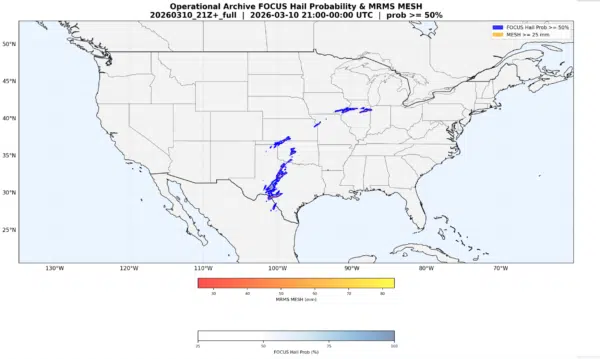

Tomorrow.io FOCUS Model — Full U.S.

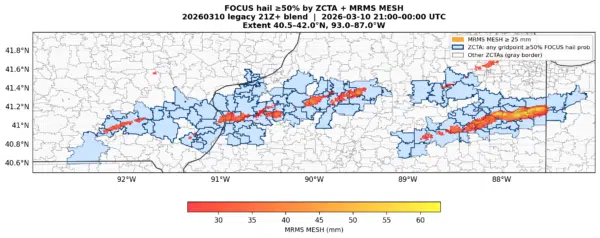

March 10, 2026: The SPC outlook covers a massive swath from Texas to Illinois. The FOCUS model isolates the specific corridors where hail probability exceeds 50%.

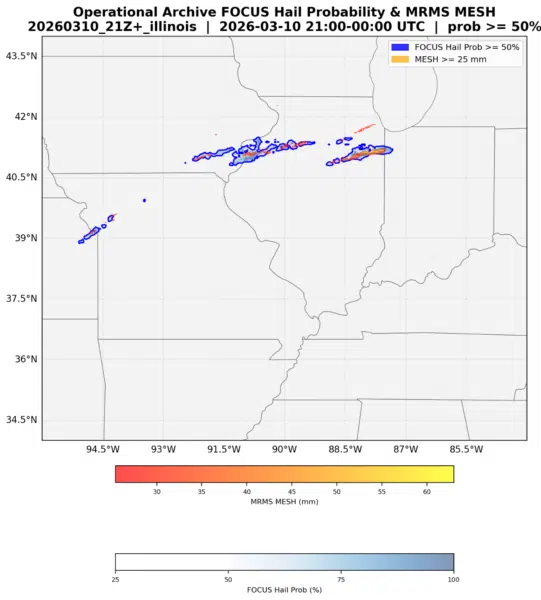

FOCUS Model — Illinois Region

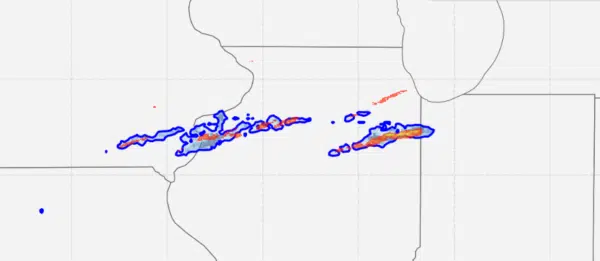

FOCUS Model — Address-Level Detail

Progressive zoom: From regional corridor to address-level precision. The blue contours show FOCUS hail probability ≥50%; orange shows MRMS-observed hail ≥25mm — confirming forecast accuracy.

The failure mode is not “bad alerts.” It is that broad-coverage advisories cannot achieve the precision needed to sustain policyholder action rates over multiple seasons. When the signal degrades, the behavioral response degrades with it — and the financial value collapses.

This is not conjecture. Peer-reviewed research quantifies the cost. Simmons and Sutter’s econometric analysis of over 20,000 tornado events found that each standard-deviation increase in false alarm ratio increases failure-to-act by 12–29% — an effect approximately equal in magnitude to providing no warning at all. When 75% of public weather warnings are false alarms, the behavioral response degrades to the point where the system is counterproductive.

Source: Simmons & Sutter, Weather, Climate, and Society, 2009.

![The Early Warning MESSAGES now Insureco Hello, [Policyholder's First Name]. This is a quick advisory from Insureco. A potentially severe hailstorm is predicted in your area tomorrow. We'll check in again tomorrow if the forecast holds and action can help protect your property. Stay alert, and we'll keep you informed if conditions change. Thank you! A primer to prep for action and soften the potential for false positive. The Imminent Action MESSAGES now Insureco [Policyholder's First Name], severe hail (over 1 inch in diameter) is forecasted to hit your area soon, between 7 p.m. and 9 p.m. today. To help prevent potential damage to your vehicle, please: Cover your car with blankets or move it into a garage or any kind of coverage. If you've taken action, reply C to confirm. Thank you for staying proactive! Sent when confident, focused on actionable timing.](https://www.tomorrow.io/wp-content/uploads/2026/04/Screenshot-2026-04-10-at-9.40.41-AM-600x292.png)

Precision is not a feature of a notification program. It is the prerequisite for one to produce financial value.

The Evidence

What a deployed pre-loss decision system produces

The forecast infrastructure

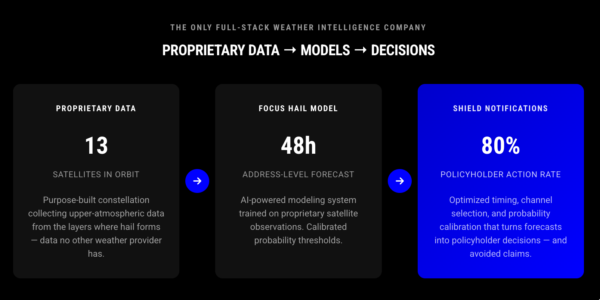

Tomorrow.io’s FOCUS model delivers a dedicated 48-hour hail forecast supported by proprietary upper-atmospheric observations from the Tomorrow Constellation — 13 satellites launched and operating, collecting data from the specific atmospheric layers where hail forms.

A new form of carrier engagement

Personal auto carriers have an engagement problem. The average policyholder interacts with their carrier twice a year — once to pay, once to file. Outside of those moments, the relationship is invisible. There is no ongoing touchpoint, no reason for the policyholder to feel that their carrier is actively working on their behalf.

This matters for retention, but it also matters for something more fundamental: the ability to influence policyholder behavior at the moment it counts. You cannot ask a customer to take protective action during a hailstorm if you have never given them a reason to listen to you before.

Shield changes this dynamic. When a carrier sends a notification 24 hours before a hailstorm — specific to the policyholder’s address, with a clear time window and a concrete action — it creates a fundamentally different kind of relationship. The carrier is no longer a company that processes paperwork after damage occurs. It is an entity that was there before the damage, actively working to prevent it.

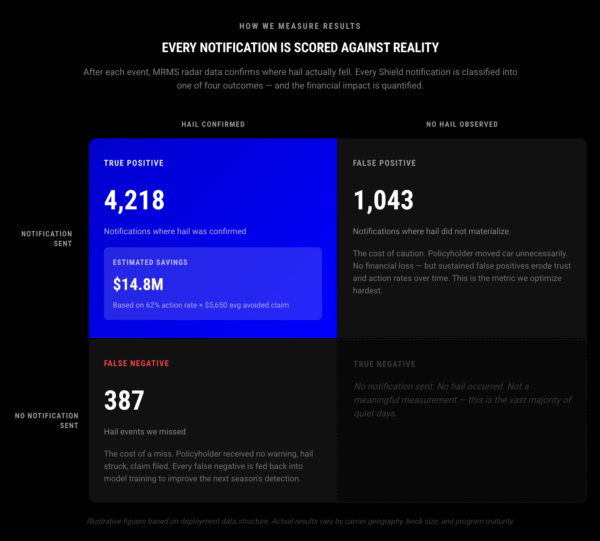

The engagement data reflects this shift. Nearly half of enrolled policyholders activate the program. More than a quarter go further — configuring their own alert preferences, choosing which perils they want to be notified about, and setting their notification channels. This is not passive receipt. It is active participation in a loss prevention program that the policyholder perceives as valuable.

7x – Industry benchmark click-through rate

49% – Program activation after enrollment

27% – Self-configure alert preferences

For context, the only other publicly quantified benchmark comes from Liberty Mutual, which reported that 44% of surveyed policyholders said an alert prompted them to take protective action — across 30,000+ enrolled customers in 21 hail-prone states — making it the only other U.S. carrier with a published behavioral outcome.

Source: Liberty Mutual press release, June 2021; Repairer Driven News.

Policyholders consistently report that it matters to them that the notification came from their carrier — not a weather app. Being there before the loss is a fundamentally different kind of relationship than being there to process it.

The avoided-claim cascade

The operational math is equally urgent. Twenty-five percent of all claims adjusters are expected to retire within five years, and catastrophe adjuster day rates now exceed $500. Every hail claim that Shield prevents doesn’t just save indemnity — it preserves bandwidth in a workforce that is structurally unable to handle current volume.

Sources: Bureau of Labor Statistics via Insurance Journal, 2025; Claims Journal, October 2025.

The System

A decision system, not a notification product

The industry is moving from detect-and-repair to predict-and-prevent. McKinsey concludes that carriers should “focus on mitigating and even preventing physical climate risk.” Deloitte estimates that $3.35 billion invested in residential resiliency measures could save insurers $37 billion by 2030.

Sources: McKinsey, “Climate Change and P&C Insurance”; Deloitte 2025 Global Insurance Outlook.

Shield is not a notification product. It is a pre-loss decision system built from five integrated components:

1. Forecast precision — FOCUS model + 13-satellite constellation delivering address-level, 48-hour hail predictions

2. Notification timing — Optimized windows that maximize the probability of policyholder action

3. Probability threshold calibration — Maintaining signal credibility over time so trust compounds, not erodes

4. Channel optimization — SMS vs. push vs. email, measured by action rate, not open rate

5. Continuous feedback loop — Post-event verification, model refinement, and campaign improvement every season

Cross-departmental value

The value extends beyond claims avoidance. For claims teams: fewer preventable events, preserved adjuster bandwidth, reduced cycle time. For underwriting: better loss ratio data in hail-exposed zones. For reinsurance: a demonstrable mitigation program to present at renewal. For retention: a fundamentally new engagement where the carrier is present before the loss.

The regulatory landscape is formalizing around this shift. NAIC announced a new Pre-Disaster Mitigation and Risk Modeling Working Group in 2026 — its first standing body dedicated to pre-event mitigation. Multiple states have already enacted mandatory premium discounts for structural mitigation programs. Carriers with deployed prevention programs will be positioned to meet whatever mitigation-credit frameworks emerge.

Source: NAIC Fall 2025 National Meeting; Sidley Austin regulatory update, December 2025.

The Opportunity

The window is open.

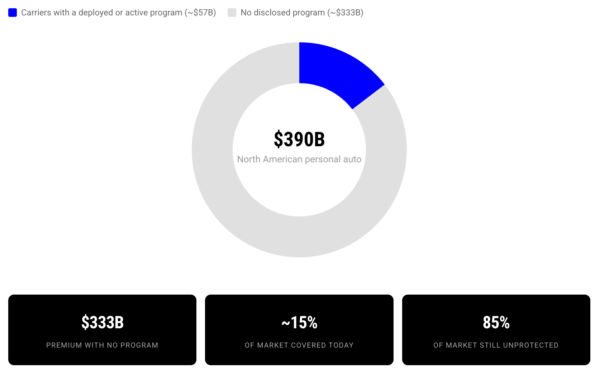

Across North America, the personal auto market represents approximately $390 billion in direct written premium. Of that, carriers representing roughly $57 billion — including several of the largest in both the U.S. and Canada — have deployed or are deploying a proactive weather notification program. The remaining $333 billion in premium has no disclosed preventative weather capability for personal auto policyholders.

Sources: NAIC 2024 Market Share Report; carrier public disclosures and program announcements as of Q1 2026.

Tomorrow.io works with carriers representing $57 billion in personal auto premium across the U.S. and Canada on preventative notification programs — and the deployment data accumulated over three years of real-world operation is the foundation of the evidence presented in this piece.

First-mover advantage

This program creates durable behavioral habits in policyholders.

Once a customer configures their alerts, trusts the signal, and acts on it — that relationship is not easily replicated by a competitor who deploys two years later.

- The engagement advantage compounds.

- The combined ratio impact compounds.

- The reinsurance positioning compounds.

This is not theoretical. A peer-reviewed study in the North American Actuarial Journal found that usage-based insurance programs improve underwriting performance only for early adopters — and only after the program matures through iterative calibration. Late entrants face a structural disadvantage.

Source: North American Actuarial Journal, Vol. 26, No. 3, 2022.

- 1 season: Q2–Q3 to measurable results

- 88–90%: Of SCS losses retained by primary carriers

Next Step

See Shield against your book

Let’s start by understanding how severe convective storms have impacted your book — and what that impact looks like through the lens of a pre-loss notification program.

March 10, 2026 — Illinois corridor. Blue polygons: zip codes where FOCUS predicted ≥50% hail probability. Orange/red: MRMS-observed hail ≥25mm. This is the overlay we build against your book.

- Select a recent hail or severe weather event from your geographic footprint

- Overlay against your claims data to establish the baseline loss

- Model the Shield notification scenario — who, when, at what confidence

- Apply conservative action rates from validated deployment data

- Quantify: claims avoided, combined ratio impact, claims bandwidth preserved

Request a meeting with Tomorrow.io

We’d love to walk you through what Shield looks like against your portfolio. No commitments — just a conversation about what’s possible.